Wedding Apparel Market - Global Industry Analysis, Size, Share, Growth, Trends, and Forecast 2018 - 2026

Wedding apparel is the dress worn by the bride and groom at a time of the wedding ceremony. Apparel style, color, and ritual are varies from one culture to another. Brides often choose white wedding apparel in the western culture, while they opt for red in the eastern culture. These colors are considered auspicious in these cultures. Wedding apparel is made of different fabrics such as silk, charmeuse, crepe, georgette, and satin. Strapless wedding dresses and wedding gowns with straps have become increasingly common in the western culture. In the eastern culture, red apparel is the traditional choice of wedding garment for brides. Besides strapless wedding apparel, long sleeves, cap sleeves, and Juliet sleeves wedding apparel are considered trendy in western countries.

The major factor which is driving the global wedding apparel market during the forecast period is rapidly developing economies with a huge number of prosperous shoppers entering the market recently. Increasing number of individuals are opting for luxury weddings in developing countries such as India and China. This is another factor boosting the wedding apparel market. Additionally, changes in lifestyle; rise in disposable income; increase in urbanization and commercialization; and fashion upgrade, especially in apparel, are augmenting the global wedding apparel market. Nowadays, people are increasingly preferring designer clothes as style statement, especially in the wedding apparel market. These factors are expected to drive the wedding apparel market during the forecasted period. However, intense competition exists in the wedding apparel market due to the presence of new entrants and competitive pricing strategies adopted by companies. This is anticipated to hamper the wedding apparel market during the forecast period.

The global wedding apparel market can be segmented based on culture type, fabric, end-user, distribution channel, and geography. In terms of culture type, the global wedding apparel market can be divided into western culture, eastern culture, and Native American culture. The eastern culture segment can be further segregated into Middle Eastern dresses, East Asian dresses, and South Asian dresses. Based on fabric, the global wedding apparel market can be classified into silk, charmeuse, crepe, georgette, satin, and others. Silk is the most ideal fabric used to make wedding apparel across the world. As compared to other fabric silk is the most hypoallergenic, lustrous beauty, and have luxurious softness. All this makes the silk fabric most attractive over the period. In term of distribution channel, the global wedding apparel market can be bifurcated into online and offline. Based on end-user, the global wedding apparel market can be divided into men and women. In terms of geography, the global wedding apparel market can be split into Middle East & Africa (GCC, South Africa, and Rest of Middle East & Africa), Asia Pacific (India, China, Japan, and Rest of Asia Pacific), North America (Canada, the U.S., and Rest of North America), Europe (the U.K., Germany, France, and Rest of Europe), and South America (Brazil and Rest of South America). Asia Pacific is anticipated to be a highly attractive region of the wedding apparel market during the forecast period. India leads the wedding apparel market in the region, as the disposable income of people in India is high compared to that in other countries in Asia Pacific.

Brochure With Latest Advancements and Application @ https://www.transparencymarketresearch.com/sample/sample.php?flag=B&rep_id=46089

Major players operating in the wedding apparel market include Pronovias, De La Cierva Y Nicolas, Jesus del Pozo, Impression Bridal, Monique Lhuillier, Vera Wang, Yolan Cris, Amsale Aberra, Rosa Clara, Pepe Botella, Victorio & Lucchino, Oscar De La Renta, White One, Carolina Herrera, TinaValerdi.com, THEIACOUTURE, Jasmine Empire, JA APPAREL CORP., Manyavar and other manufacture are planning to enter into the global wedding apparel market.

The report offers a comprehensive evaluation of the market. It does so via in-depth qualitative insights, historical data, and verifiable projections about market size. The projections featured in the report have been derived using proven research methodologies and assumptions. By doing so, the research report serves as a repository of analysis and information for every facet of the market, including but not limited to: Regional markets, technology, types, and applications.

Download Report TOC for in-depth analysis @ https://www.transparencymarketresearch.com/sample/sample.php?flag=T&rep_id=46089

Dock Finger Market - Global Industry Analysis, Size, Share, Growth, Trends, and Forecast 2018 - 2026

Dock finger is a floating pontoon that separates the boats and offers access to berthed boats in a marina and provides mooring line attachment points. These structures are primarily used in marine bays with respect to tidal variation or other occurrences affecting the water level. Dock fingers are also employed in boating centers and yacht clubs for coastline protection and development. These are generally made from rot-resistant materials or wood walkways that are reinforced by aluminum framework resting on air-filled chambers made of laminate material. Some dock fingers are also made using modular plastic units without any additional structure. Utilization of standard fasteners allow reorganization and reconfiguration of modules at marine facilities. Some dock fingers are also equipped with lighting pedestals and have bollards, cleats, and/or mooring rings. Dock fingers can also be anchored with the help of anchor chains linked to a master chain. Some dock fingers are held in place with the help of pilings, a system that allows dock fingers to slide up and down with changing water levels.

The global dock finger market is expected to expand at a considerable pace. Growing housing industry alongside beaches (man-made and natural) is expected to be a key factor driving the dock finger market. Customers are buying residential or commercial properties alongside beaches and man-made or natural islands are expected to require dock fingers to dock boats and yachts. Increase in public private partnerships (PPP) to construct man-made islands is anticipated to boost the market. The best example of a man-made island is the Palm Jumeirah located in Dubai where a large number of dock fingers are available to dock ships and yachts. Extensive usage of dock fingers in the commercial sector such as beach side hotels, resorts, and ports is expected to fuel the dock finger market. Additionally, increase in sales of yachts, motor boats, power boats, jet-skis, and electric and hybrid boats is anticipated to propel the dock finger market. However, high cost of docks finger and high maintenance cost are expected to restrain the global dock finger market. Additionally, lack of proper infrastructure for setting up dock fingers is projected to hamper the market. However, government initiatives to improve port facilities is expected to create opportunities in the global dock finger market. Moreover, increase in cross country trade through waterways is expected to boost the market. Cross country trade is also anticipated to help develop dock fingers in potential markets.

Brochure With Latest Advancements and Application @ https://www.transparencymarketresearch.com/sample/sample.php?flag=B&rep_id=47379

Companies, in order to gain an edge over their competitors, are coming up with dock fingers for various water sports. For example, Cadock, a Canada-based dock finger company manufactures diverse dock finger products based on water sports such as jet ski floating docks and rowing floating docks. The global dock finger market can be segmented based on product type, material type, end-use, industry, and geography. In terms of product type, the market can be classified into modular, floating, and fixed. Based on material type, the market can be categorized into metal, concrete, plastics, and others (wooden, etc.). In terms of end-use, the dock finger market can be classified into mooring, drive-on, and work. Based on industry, the market can be divided into commercial, residential, government, and industrial. In terms of geography, the global dock finger market can be segmented into North America, Europe, Asia Pacific, Middle East & Africa, and South America. Prominent players operating in the global dock finger market include A-Laiturit, CANDOCK, Ingemar, Clement Germany, Karl Innovation, Marina Dock Systems, MarineMaster, Metalu Industries, MARTINI ALFREDO, Orsta Marina, Poralu Marine, Potona Marine, Ronautica, Technomarine Manufacturing, Yacht Port Marinas.

The report offers a comprehensive evaluation of the market. It does so via in-depth qualitative insights, historical data, and verifiable projections about market size. The projections featured in the report have been derived using proven research methodologies and assumptions. By doing so, the research report serves as a repository of analysis and information for every facet of the market, including but not limited to: Regional markets, technology, types, and applications.

Download Report TOC for in-depth analysis @ https://www.transparencymarketresearch.com/sample/sample.php?flag=T&rep_id=47379

Adoption of Integration Platform as a Service (IPaaS) in Healthcare Industry to Increase through 2022

The advent of integration technologies and their ongoing evolution exhibits a disruptive impetus across multiple industrial verticals. However, such disruptions are turning out to be profitable for companies and organizations seeking to integrate their applications and business platforms. Cloud networking and cloud computing are being extensively exercised across several industrial domains. As such technologies are penetration beyond technology-based businesses, the need for integrating their functionalities is becoming crucial.

According to a recent report published by Transparency Market Research, factors as such are fuelling the adoption of Integration Platform as a Service (IPaaS) in the world. In the near future, IPaaS will be actively adopted by enterprises seeking to integrate data and on-premise applications for propelling business growth. By allowing users an effective connectivity across multiple applications, IPaaS platforms are enabling employees of an enterprise deploy such integrations without installing an additional hardware or software.

By the end of 2022, the global market for Integration Platform as a Service is estimated to reach US$ 1.2 valuation. The study anticipates that during the five-year forecast period, 2017-2022, the global IPaaS market will have soared robustly at a CAGR of 11.9%. The report also projects that North America will be the largest market for IPaaS in the immediate future.

North America to Represent Leading Market for IPaaS

Key findings from the regional analysis availed in the report reveal that North America will be at the forefront of expansion of the global IPaaS market over the forecast period. By the end of 2022, North America’s IPaaS market is anticipated to worth nearly half a billion dollars. The report also anticipates considerable adoption of IPaaS in European markets. Through 2022, the IPaaS market in Europe is poised to soar at a CAGR of 11.4%. Although, the fastest adoption of IPaaS is likely to be recorded in the Asia-Pacific excluding Japan (APEJ) market. Over the forecast period, the APEJ IPaaS market is expected to grow vigorously at over 13% CAGR.

Get PDF Sample for this Research Report @ https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=31469

Healthcare and Education Industries to Exhibit Steadfast Adoption

Among the key industries, healthcare and education are anticipated to showcase a surging growth in terms of adoption of IPaaS solutions. Pharmaceutical companies are likely to implement IPaaS for boosting the efficiency of manufacturing applications and integrating production data with sales registries. Educational organizations are also anticipated to adopt these services and increase integration of learning processes with interactive devices and applications. The report also reveals that through 2022, the adoption of IPaaS will remain predominant in the IT & telecommunications industry.

With respect to end-users, large enterprises are anticipated to dominate the global IPaaS market, while small & medium enterprises will witness an impressive traction in terms of adopting IPaaS. On the basis of components, the global IPaaS market is bifurcated into software platforms and services, with the former segment representing higher share on global revenues. The report anticipates that adoption of IPaaS services is low at present, albeit, it will surge towards the end of 2022, considering the increasing complexities of implementing software platforms in the absence of proper deployment services.

The report has profiled leading IPaaS providers as key market players, which include IBM Corporation, Oracle Corporation, MuleSoft, Inc., Red Hat, Inc., Fujitsu Ltd., Microsoft Corp., SAP SE, Capgemini SE, Dell Inc., and TIBCO Software Inc. These companies are expected to remain active in the expansion of global IPaaS market through 2022.

Download Report TOC for in-depth analysis @ https://www.transparencymarketresearch.com/report-toc/31469

China Condom Market to touch US$5.04 bn by 2024

The condoms market in China features a high level of consolidation, with the top three companies accounting for over 70% share in the overall market in 2015, states Transparency Market Research (TMR) in a recent report. These three companies, Reckitt Benckiser Group plc, Ansell Ltd., and Church and Dwight Co., command a prominent position in the overall growth dynamics of the China condoms market, giving a tough competition to local manufacturers.

To strengthen their position in the market amid the intense level of competition, companies such as Reckitt Benckiser Group plc have resorted to the development of innovative products and newer ways of marketing to knock off the threat of counterfeit products and high advertisement and distribution costs. The company shifted to an all-digital and all social strategy post 2010, which helped the company to increase its share in the overall market from 30% in 2010 to 45.6% by 2015.

Get PDF Sample for this Research Report @ https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=13898

Rising Awareness about Efficacy in Controlling Sexually Transmitted Diseases to Boost Adoption

Condoms have gained an increased level of acceptance in China after the government actively started endorsing condoms as an effective way of preventing sexually transmitted diseases such as HIV/AIDS and Chlamydia. Prior to 2002, condoms were endorsed by the government as a hygiene concept, leading to a marketplace with narrow growth opportunities. With rise in active initiatives by the government aimed at educating the masses about the importance of safe sex, the sales of condoms have substantially increased.

Apart from this factor, the improving quality of lifestyles, driven by a strengthening economy, and the rising know-how about safer ways of preventing contraception and sexually transmitted diseases have also worked substantially in favor of the country’s condom’s market. Sales of a variety of condoms have also increased in the country owing to factors such as the rising popularity of female condoms, rise in the country’s sexually active demographic, and increase in usage of homosexual condoms.

Condom Sales Face Rough Weather as China Ends One Child Policy

Ever since the announcement that China had ended the one child policy was made at the beginning of 2015, manufacturers of condoms had been dreading reduction in the overall sales of condoms in the country. The fears did not turn out to be insignificant and key vendors operating in the China condoms market started witnessing a slump in demand. By the end of 2015, Okamoto Industries saw a dip in its market share by 24%, Female Health witnessed a decline of 19% and shares of Church and Dwight dropped by 3%.

Download Report TOC for in-depth analysis @ https://www.transparencymarketresearch.com/report-toc/13898

Though the present-day impact of this factor is tremendous on the market, the trend is expected to have a low impact on the overall condoms market in the long-run. Analysis estimates that the awareness regarding protective properties of condoms will work more in favor of the China condom market in the long run than how the end of the one-child-policy is negatively impacting sales currently.

Customer Communication Management Market to reach US$1.06 bn by 2025 - TMR

The U.S. over the years has remained one of the early adopters of the latest technologies. On account of this, the demand for customized communication solutions is considerably high, rendering the U.S. customer communication management (CCM) market highly competitive. As the existing retailers enjoy a strong presence, the market doesn’t provide much scope for the entry of new players, finds Transparency Market Research (TMR) in a new study. In addition, the market is reeling under the availability of substitutes, which makes sustenance of market share difficult key players.

“Considering the scenario, the leading CCM vendors are focusing on offering diverse customized solutions by developing and integrated CCM software with cloud environment,” said a lead TMR analyst. Also the presence of several large companies has exacerbated the prevailing competition. Currently, companies such as HP Enterprises, Pitney Bowes Inc., OpenText Corp., and Adobe Systems Incorporated hold strong position in the U.S. customer communication management market. Together these companies held the dominant share of 30.6% in the U.S. CCM market in 2016.

Market")

Furthermore, Oracle Corporation, EMC Corp. (Dell), and Cincom Systems, Inc., are among the other prominent vendors in the U.S. CCM market. According to TMR, the U.S. CCM market stood at US$423.1 mn in 2016. Rising at a CAGR of 11% between 2017 and 2025, the market is forecast to reach US$1.06 bn by the end of 2025. Among various solutions available in the market, software suite held the dominant share of 46.9% in the overall market in 2016. By end use, the IT & Telecom emerged as the lead holding over 20.5% of the market in the same year. The aforementioned segments are also expected to remain dominant through the course of the forecast period.

Brochure With Latest Advancements and Application @ https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=21809

Demand for Multifarious Communication Channels to Drive Growth

Customer communication has become more dynamic with the advent of ground-breaking communication channels. These innovations over the last few years and knowledge about benefits they offer have brought organizations to their feet. They are now keener on multifarious communication channels to establish their presence across diverse platforms as these technologies have empowered them to connect with customers in any corner of the world. Consequently, the demand for customer communication management is accelerated and the trend is less likely to slow down any time soon.

It is important to note that the U.S. is a relatively mature market. The enterprises operating from this nation are therefore more interested in batch, interactive and on-demand communication solutions. This is further triggered by the rising demand for solutions that will help organizations acquire, serve, and grow customer relationship. As on-demand CCM systems support non-linear development model, they help organizations rationalize messy application platforms. This is one of the key factors driving the customer communication management market in the U.S. In addition, the rising emphasis on context-rich information and multi-channel output will impel companies invest more in advanced customer communication management solutions.

Download Report TOC for in-depth analysis @ https://www.transparencymarketresearch.com/report-toc/21809

Security Concerns Related to CCM Software may Hamper Growth

On the flip side, security concerns related to CCM software could act against the market in the near future. Sectors such as BFSI, government, healthcare, and retail require robust customer interaction platform. While CCM software caters to the requirement, it is yet to eliminate a few inherent security concerns that comes with the technology. This could hinder the market’s trajectory to an extent.

Nevertheless, the evolution of the CCM software technology to cloud will facilitate the deployment of communication software without much complexity or incurring huge expense. “The evolution of cloud-based environment will enable customer communication management software to cater to small, medium, as well as large enterprises,” observed the TMR report’s author. This will open lucrative opportunities for the market’s growth in the near future.

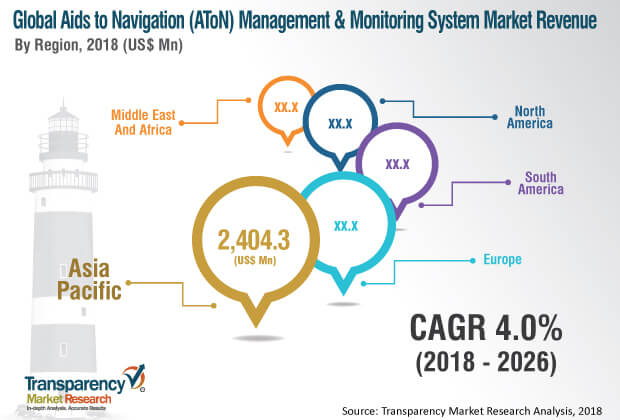

Aids to Navigation (AtoN) Management and Monitoring Systems Market to Reach US$ 9,075.1 Mn

According to a new market report pertaining to the Aids to Navigation AtoN Management and Monitoring System Market published by Transparency Market Research, the AtoN management and monitoring system market is projected to reach US$ 9,075.1 Mn in 2026, driven by a rise in marine trade across the globe. The market is projected to expand at a CAGR of 4.0% during the forecast period from 2018 to 2026. The expansion of the market is attributed to high coastal security concerns and demand for AtoN management and monitoring systems from the defense sector. Asia Pacific is anticipated to lead the AtoN management and monitoring system market, followed by Europe and South America, during the forecast period.

Request PDF Sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=52101

Rise in Marine Trade is Likely to Drive the Market

Increasing marine trade activity across the globe is creating significant demand for marine safety and security and marine traffic management. A rise in marine trade increases the need for appropriate navigation, continuous monitoring of vessels and routes, and managing traffic. All these factors contribute to the growth of the AtoN management and monitoring system market across the world.

VHF-based data exchange systems (VDES) provide a robust and global standard communication system for e-navigation, supporting the safety and efficiency of ship and shore operations. An increase in marine trade is expected to exert pressure on existing navigational tools.

AtoN Management and Monitoring System Market: Scope of the Report

The AtoN management and monitoring system market has been segmented based on system, type, navigation components, end-use industry, and region. In terms of system, the integrated systems segment is expected to dominate the global market in 2018.

Asia Pacific led the AtoN management and monitoring system market, accounting for a substantial share in 2017. China was a major country of the AtoN management and monitoring systems market in the region. The AtoN management and monitoring system market in North America, Europe, Middle East & Africa, and South America is also expected to expand during the forecast period.

Download Report TOC for in-depth analysis @ https://www.transparencymarketresearch.com/report-toc/52101

AtoN Management and Monitoring System Market: Competitive Dynamics

The research study includes profiles of leading companies operating in the global AtoN management and monitoring system market. Key players profiled in the report include Tideland, GISMAN, McMurdo Group, i-Marine Technologies, Pharos Marine Automatic Power Inc., Navielektro, Greenfinder, Carmanah Technologies Corp., Vesper Marine, and Pinc Technology Sdn Bhd..

Demand for Digitally Advanced Services From Tech-savvy Consumers to Drive U.S. Quick Service Restaurant (QSR) IT Market, reports TMR

The presence of a large number of software companies offering distinguished services to the quick service restaurant (QSR) industry in the U.S. has made the U.S. QSR IT market highly competitive, reports Transparency Market Research (TMR) in a recent report. The top five vendors in the market collectively accounted for a mere 25% in the overall market in 2015. To gain an edge, IT services and solutions providers for the QSR industry in the U.S. are continuously innovating and developing products capable of reducing turnaround times of services.

Innovations that can hit the right note with the country’s tech savvy consumers, making their dining experience not only quick but also memorable, are also being increasingly sought. Vendors in the market are creating long-term partnerships with large- and mid-sized QSRs to gain sustained returns in the intensely competitive market. The provision of IT solution in a single package or bundled services, with monthly or annual payment packages, is also emerging as a prominent trend in the U.S. QSR IT market.

Some of the key vendors operating in the market are NEC Display Solutions of America, Inc., Panasonic Corporation, HM Electronics, Inc., Oracle Corporation, NCR Corporation, PAR Technology Corporation, and Revel Systems, Inc.

Get PDF Sample for this Research Report @ https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=13919

IT Market")

Rising Hourly Wages in the U.S. Trigger Adoption of QSR IT Solutions

The U.S. Bureau of Labor Statistics finds that the average hourly earnings of people working in the food services industry has increased from nearly US$11.54 in 2010 to US$13.33 in 2016. This trend in salary inflations is a prominent factor compelling QSR owners in making the shift from manual operations to machine-based automatic operations. In the next few years, IT solutions that can replace the need for manual intervention in QSR operations, such as digital kiosks, tabletop e-waiters, digital checkout counters, and digital menu boards will gain increased adoption. Hand-held devices, especially, such as tablets and smartphones, will gain increasingly prominent positions in the future IT-enabled QSR infrastructures.

Download Report TOC for in-depth analysis @

https://www.transparencymarketresearch.com/report-toc/13919

Need for Speed in Consumer Services to Stimulate Demand

With a continuous rise in the numbers of quick service restaurants in the U.S., the competition has also soared. Hence, ways of delivering best-in-class services and meeting consumer expectations are being pursued. This has driven the increased adoption of digital channels for transacting in quick service restaurants in the past few years in the U.S. market. QSRs in the country are updating their internal systems to make meal orders and payments compatible with near field communication and mobile wallets. Contactless payment solutions, which can immensely help smoothen transactions, are increasingly being tested by payment solution providers for creating quick payment options.

In the next few years, the rising number of smartphones users in the country is expected to make smartphones the central point of contact with consumers for the QSR industry. Thus solutions enabling purchasing, ordering, and payment using smartphones will be the most promising revenue generators.